Off-Ramping to AUD in Australia: USDT/USDC to Bank

USDC and USDT are widely used by Australian businesses to receive fast, predictable payments. Off-ramps enable businesses to settle stablecoin payments into Australian dollars (AUD), moving funds from on-chain settlement to local bank accounts in a compliant and operationally simple way. This guide explains what off-ramps are, how off-ramping works in Australia, and why it plays a critical role in modern business payment workflows.

Australian businesses use off-ramps to receive AUD from stablecoin payments and manage cash flow within compliant financial operations.

%201.png)

Nominated for 'Financial Services Innovator of the Year'

What is an Off-Ramp?

An off-ramp is a payment service that enables businesses to settle stablecoin funds into Australian dollars (AUD) and receive those funds into a local bank account.

For Australian businesses accepting payments in USDC or USDT, a crypto off-ramp acts as the bridge between on-chain settlement and the domestic banking system. Rather than holding stablecoins indefinitely, businesses can withdraw AUD as part of their normal cash-flow operations.

Off-ramps are commonly used for operational purposes such as payroll, tax obligations, supplier payments, and general business expenses that require AUD.

What Off-Ramps Do in a Payment Workflow

In a stablecoin payment workflow, off-ramps handle the final settlement stage. After a business receives a payment on-chain, the off-ramp facilitates the withdrawal of funds to AUD through compliant banking rails.

Rather than functioning as a trading or exchange mechanism, an off-ramp focuses on:

- Settlement

- Payout

- Compliance

- Reporting

This distinction is important for businesses that require predictable outcomes, transparent records, and alignment with Australian regulatory expectations.

Off-ramps allow businesses to treat stablecoin payments as part of their standard financial operations, rather than as speculative or trading activity.

Why Off-Ramping Matters for Australian Businesses

Off-ramping is a critical part of how Australian businesses operationalise stablecoin payments. While stablecoins enable fast and predictable on-chain settlement, off-ramps allow businesses to receive AUD, manage cash flow, and meet local financial obligations within the Australian banking system.

For businesses using stablecoins as a payment rail rather than a speculative asset, off-ramps provide the connection between global digital payments and day-to-day operations.

Predictable Cash Flow

Off-ramps enable businesses to withdraw AUD on demand, allowing stablecoin payments to be incorporated into normal cash-flow planning without exposure to market timing or price volatility.

Operational Simplicity

By settling stablecoin payments into AUD, businesses can continue paying staff, suppliers, and tax obligations using familiar banking rails, accounting systems, and financial processes.

Regulatory Alignment

Off-ramps operate within Australia’s AML/CTF framework, ensuring identity verification, transaction monitoring, and reporting obligations are met when stablecoin payments move into the banking system.

Reliable Business Payouts

Rather than relying on correspondent banking or international transfers, off-ramps provide a direct and predictable pathway from on-chain settlement to Australian bank accounts.

How Off-Ramps Work in Australia

In Australia, off-ramps provide the operational layer that moves stablecoin payments from on-chain settlement into the domestic banking system. Rather than functioning as a trading venue, an off-ramp focuses on compliant payout, reporting, and reconciliation so businesses can receive AUD into a local bank account.

This allows businesses to use stablecoins as a payment rail while continuing to run payroll, tax, and supplier workflows in AUD.

On-Chain Payment Receipt

A customer pays in USDC or USDT to your business wallet address. The payment settles on-chain, creating a timestamped record that can be referenced for reconciliation.

Payout Request and Matching

A payout is initiated to move funds from stablecoins into AUD. The off-ramp validates the request, confirms beneficiary details, and matches the payout against compliance requirements and reporting rules.

Compliance Checks

Off-ramps operating in Australia follow AML/CTF obligations. Identity verification, transaction monitoring, and record-keeping help ensure stablecoin payouts align with Australian regulatory expectations.

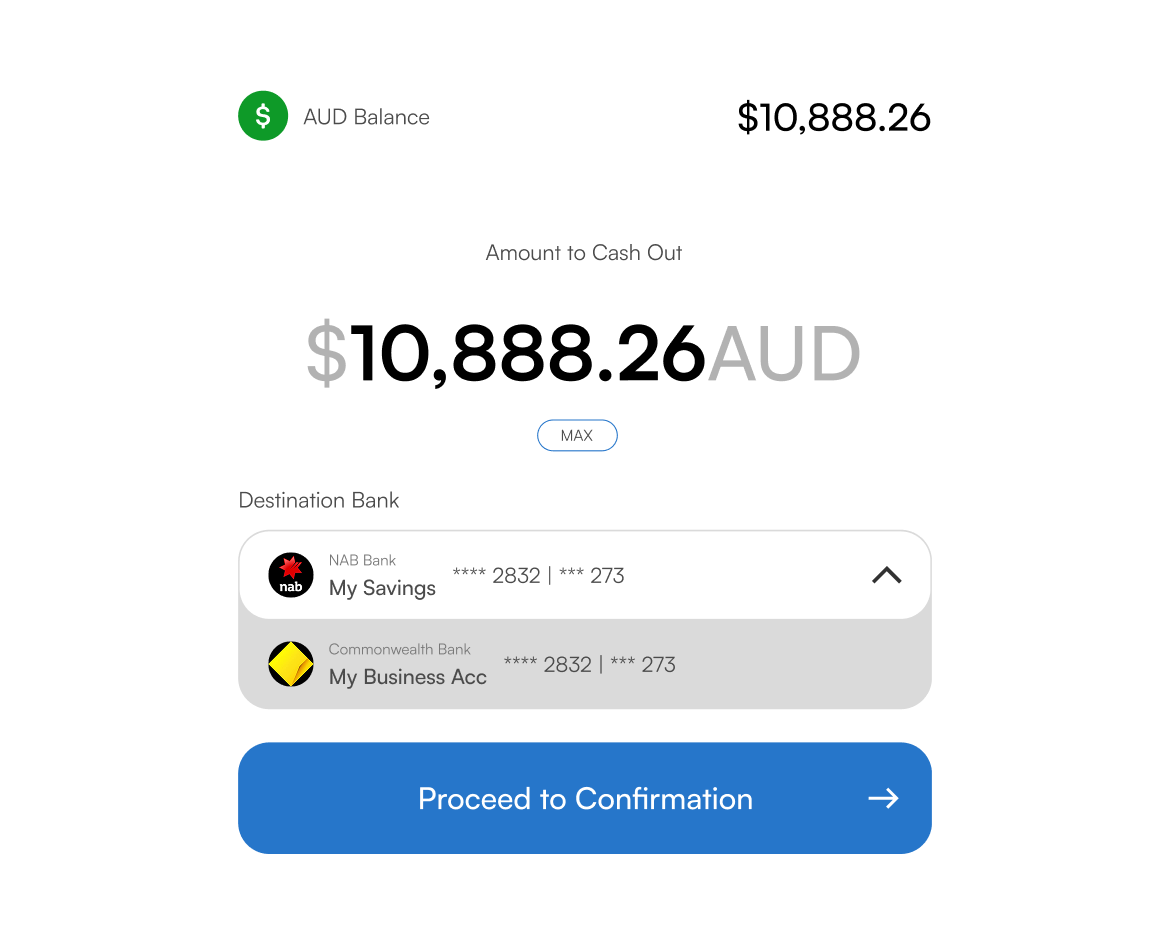

AUD Payout to Local Bank Accounts

Once approved, the off-ramp issues an AUD payout to the nominated Australian bank account. This creates a predictable outcome for cash flow and day-to-day operating costs.

Transparent Reporting

A structured payout record links the on-chain payment to the AUD outcome. This supports bookkeeping, invoice matching, and audit trails without relying on screenshots or manual tracking.

Operational Use (Not Trading)

The goal is not speculation. Off-ramps exist to support business operations by providing a compliant path from stablecoin receipts to AUD that can be used for payroll, suppliers, and taxes.

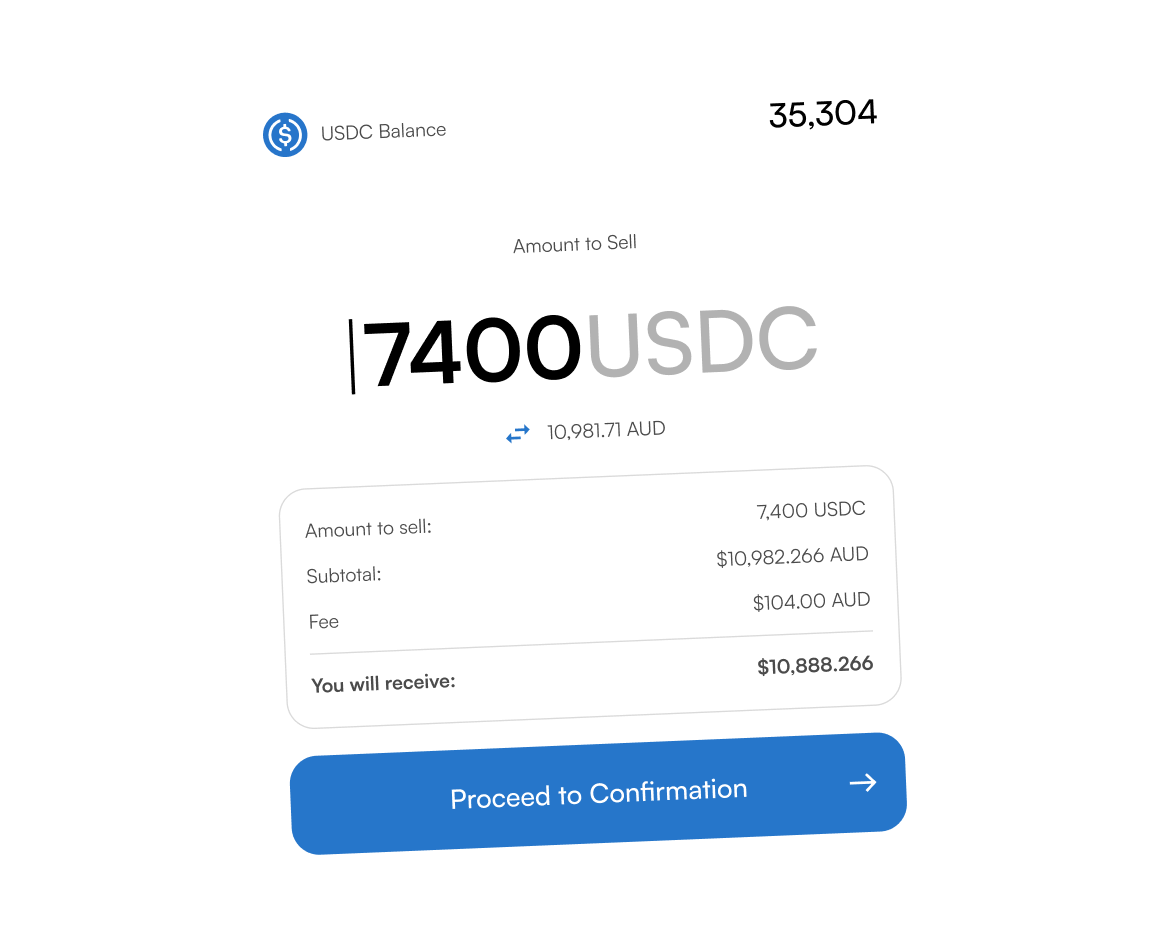

Off-Ramping Stablecoins to AUD

Off-ramping allows Australian businesses to move stablecoin payments from on-chain settlement into Australian dollar (AUD) bank accounts. This step bridges digital payment rails with domestic financial operations, enabling businesses to manage cash flow, meet local obligations, and operate within familiar banking systems.

Why Businesses Off-Ramp Stablecoin Payments

Businesses off-ramp stablecoins when they need AUD liquidity for payroll, tax obligations, supplier payments, or general operating expenses. While stablecoins are effective for receiving payments globally, most day-to-day business costs in Australia are settled in AUD.

Off-ramping provides a predictable and compliant way to transition from digital settlement to local cash management without disrupting existing financial workflows.

How Off-Ramping Fits Into Business Operations

In practice, businesses receive payments in USDC or USDT on-chain and decide when to initiate an AUD payout based on operational needs. Some businesses off-ramp immediately, while others retain stablecoins temporarily before settling to AUD.

This flexibility allows organisations to separate payment receipt from payout timing, supporting smoother cash-flow planning and operational control.

When Off-Ramping Provides the Most Value

- Paying Australian staff, contractors, or suppliers

- Meeting tax and regulatory obligations in AUD

- Managing recurring operating expenses

- Smoothing cash-flow timing between inbound payments and outbound costs

- Reducing reliance on international banking transfers

In these situations, off-ramping enables businesses to treat stablecoin payments as part of a standard financial workflow, rather than a standalone digital asset process.

USDC and USDT Off-Ramps

USDC and USDT are the most commonly used stablecoins for business payments in Australia. Both are designed to maintain a stable value while enabling fast, on-chain settlement for domestic and international transactions.

Off-ramps provide the operational layer that allows businesses to move from receiving USDC or USDT on-chain to settling Australian dollars (AUD) into local bank accounts as part of normal financial operations.

Why Businesses Use USDC and USDT

Australian businesses typically use USDC and USDT because they offer predictable settlement outcomes and broad compatibility across wallets, payment infrastructure, and blockchain networks.

USDC and USDT are commonly used for:

Receiving payments from international clients

Settling invoices without banking cut-off times

Managing predictable payment amounts without price volatility

Operating alongside existing accounting and reconciliation processes

Both stablecoins function as payment rails rather than speculative assets in commercial workflows.

How USDC and USDT Off-Ramps Fit Into Operations

In practice, businesses receive payments in USDC or USDT to a designated wallet address. When AUD liquidity is required, an off-ramp enables settlement into an Australian bank account through compliant banking rails.

Some businesses off-ramp immediately after receiving payment, while others retain stablecoins temporarily to manage cash-flow timing. This separation between payment receipt and payout allows greater operational control without changing how customers pay.

When USDC vs USDT Is Typically Used

USDC is often preferred for its transparency, regular reserve disclosures, and alignment with regulated financial institutions.

USDT is widely used due to its liquidity, global adoption, and compatibility across payment platforms and regions.From an operational perspective, both stablecoins can support compliant off-ramping into AUD when used within appropriate regulatory frameworks.

In all cases, off-ramps enable businesses to treat stablecoin receipts as part of a standard financial workflow rather than a standalone digital asset process.

Off-Ramp Regulation in Australia

Australia permits the use of stablecoins such as USDC and USDT for commercial payments, provided they operate within existing financial and digital asset regulations. While there is no standalone stablecoin law, off-ramping activity is regulated under Australia’s broader AML/CTF and financial services framework.

Australian regulators have taken a measured, principles-based approach that focuses on compliance, transparency, and financial system integrity rather than restricting legitimate business use.

AUSTRAC and AML/CTF Requirements

Off-ramp service providers operating in Australia are required to comply with the Anti-Money Laundering and Counter-Terrorism Financing (AML/CTF) Act. This includes obligations such as:

- Customer identity verification (KYC)

- Ongoing transaction monitoring

- Record-keeping and auditability

- Reporting of suspicious or threshold transactions

These controls ensure that stablecoin payouts into AUD are traceable, compliant, and aligned with Australia’s financial crime prevention standards.

Role of Banks and Payment Rails

When stablecoins are off-ramped into AUD, funds move through regulated domestic banking rails. This ensures payouts are subject to the same oversight, reconciliation standards, and reporting expectations as other electronic payments within the Australian banking system.

This structure allows businesses to integrate stablecoin payments into existing financial operations without bypassing regulatory safeguards.

Government and Regulatory Direction

Australian government bodies, including the Treasury and the Reserve Bank of Australia (RBA), have publicly acknowledged the potential benefits of well-regulated stablecoins for payments and settlement efficiency.

Ongoing consultations focus on reserve quality, transparency, and operational standards, signalling support for compliant stablecoin usage while discouraging unbacked or opaque models.

What This Means for Australian Businesses

For businesses operating in Australia, this regulatory environment means:

- Stablecoins can be accepted for commercial payments

- AUD payouts must occur via compliant off-ramp providers

- Reporting and compliance requirements are handled at the infrastructure level

- Stablecoin payments can be treated as part of standard financial workflows

This framework enables businesses to use stablecoins confidently while remaining aligned with Australian regulatory expectations.

Frequently Asked Questions on Stablecoins

An off-ramp is a service that allows businesses to withdraw stablecoin payments into Australian dollars (AUD) via compliant banking rails. It connects on-chain settlement with the domestic financial system.

Yes. Australian businesses can legally receive stablecoins such as USDC and USDT for commercial payments, provided they operate within existing financial and AML/CTF regulations.

Businesses use off-ramps when they need AUD liquidity for payroll, tax obligations, supplier payments, rent, or other domestic operating expenses.

Yes. Businesses can receive payments on-chain and decide when to initiate an AUD payout based on operational needs and cash-flow planning.

Yes. Off-ramp providers operating in Australia must comply with AML/CTF obligations, including identity verification, transaction monitoring, and record-keeping.

No. Off-ramps work alongside existing bank accounts by enabling compliant AUD payouts from stablecoin payments into local Australian accounts.

Off-ramps are commonly used by exporters, digital service providers, consultants, SaaS companies, agencies, and businesses with international clients.

No. Off-ramps are designed for operational use, allowing businesses to treat stablecoin payments as part of standard financial workflows rather than speculative activity.

Stablecoin Glossary

Algorithmic Stablecoin

A stablecoin that maintains value using software-based supply adjustments instead of external reserves. Algorithms expand or contract supply based on market conditions to keep the token near its target price.

AML/CTF Compliance

Anti-Money Laundering and Counter-Terrorism Financing regulations that apply to stablecoin service providers in Australia. Businesses must follow reporting, monitoring, and verification obligations under AUSTRAC.

Attestation / Audit

A third-party verification of stablecoin reserves. These reports confirm whether each issued token is properly backed by cash, cash-equivalents, or collateral.

Blockchain Network

A decentralised digital ledger that records stablecoin transactions securely and transparently. Public blockchains allow global settlement without traditional banking rails.

Burning

The process of permanently removing stablecoin tokens from circulation, typically when they are redeemed for their underlying asset.

Collateralisation

The mechanism of backing stablecoins with reserves or assets. Stablecoins may be fully collateralised, partially collateralised, or over-collateralised depending on design.

Correspondent Banking

A traditional cross-border payment system involving intermediary banks. Stablecoins bypass this model, enabling faster global settlement.

Crypto-Backed Stablecoin

A stablecoin backed by other digital assets rather than fiat currency. These stablecoins are typically over-collateralised and managed by smart contracts. Example: DAI.

Custodial Wallet

A digital wallet where a third-party provider manages and stores private keys on behalf of the user. This simplifies usage for businesses that prefer managed security.

DeFi (Decentralised Finance)

A blockchain-based financial ecosystem that uses stablecoins for lending, borrowing, trading, and liquidity provision without traditional intermediaries.

Digital Asset

Any asset issued, stored, or transferred on a blockchain, including stablecoins, cryptocurrencies, and tokenised representations of real-world assets.

Fiat-Backed Stablecoin

A stablecoin backed 1:1 by cash or cash-equivalents held by a regulated custodian. These are the most commonly used stablecoins in Australia. Examples: USDT, USDC.

KYC (Know Your Customer)

A verification process required by AUSTRAC to confirm user identity before enabling stablecoin payments, withdrawals, or conversions.

Liquidity

The ease with which a stablecoin can be exchanged for cash, other digital assets, or used in transactions without affecting its market price.

Minting

The creation of new stablecoin tokens, typically triggered when a user deposits equivalent fiat or collateral into a stablecoin system.

Non-Custodial Wallet

A wallet where users control their own private keys, offering greater autonomy and security responsibility.

On-Chain Settlement

The finalisation of transactions directly on the blockchain. Stablecoin settlement typically completes within seconds or minutes, regardless of location.

Over-Collateralisation

Providing more collateral than the value of stablecoins issued. Used to protect crypto-backed stablecoins from price volatility.

Peg

The target value a stablecoin aims to maintain, commonly set to a fiat currency such as 1 USD.

Programmable Money

Stablecoins used within smart contracts or automated workflows, enabling rules-based payments, invoicing, or settlement without manual intervention.

Redemption

The process of exchanging stablecoins back into fiat currency or underlying collateral through an issuer or liquidity provider.

Reserve Assets

Cash, cash-equivalents, and other high-quality liquid assets held to back fiat-backed stablecoins and maintain their 1:1 peg.

Settlement

The confirmation and completion of a transaction. Stablecoin settlement is typically near-instant and recorded on-chain.

Smart Contract

Self-executing code deployed on a blockchain that automates stablecoin minting, collateral management, interest calculations, or other financial processes.

Stablecoin

A digital asset engineered to maintain a stable value, typically pegged to a fiat currency like USD. Used for payments, invoicing, settlement, and global value transfer.

PLATFORM

Features Focussed on

Getting You Your Money

Simple to use, powerful and fast under the hood - FastStables is built for your end goal.

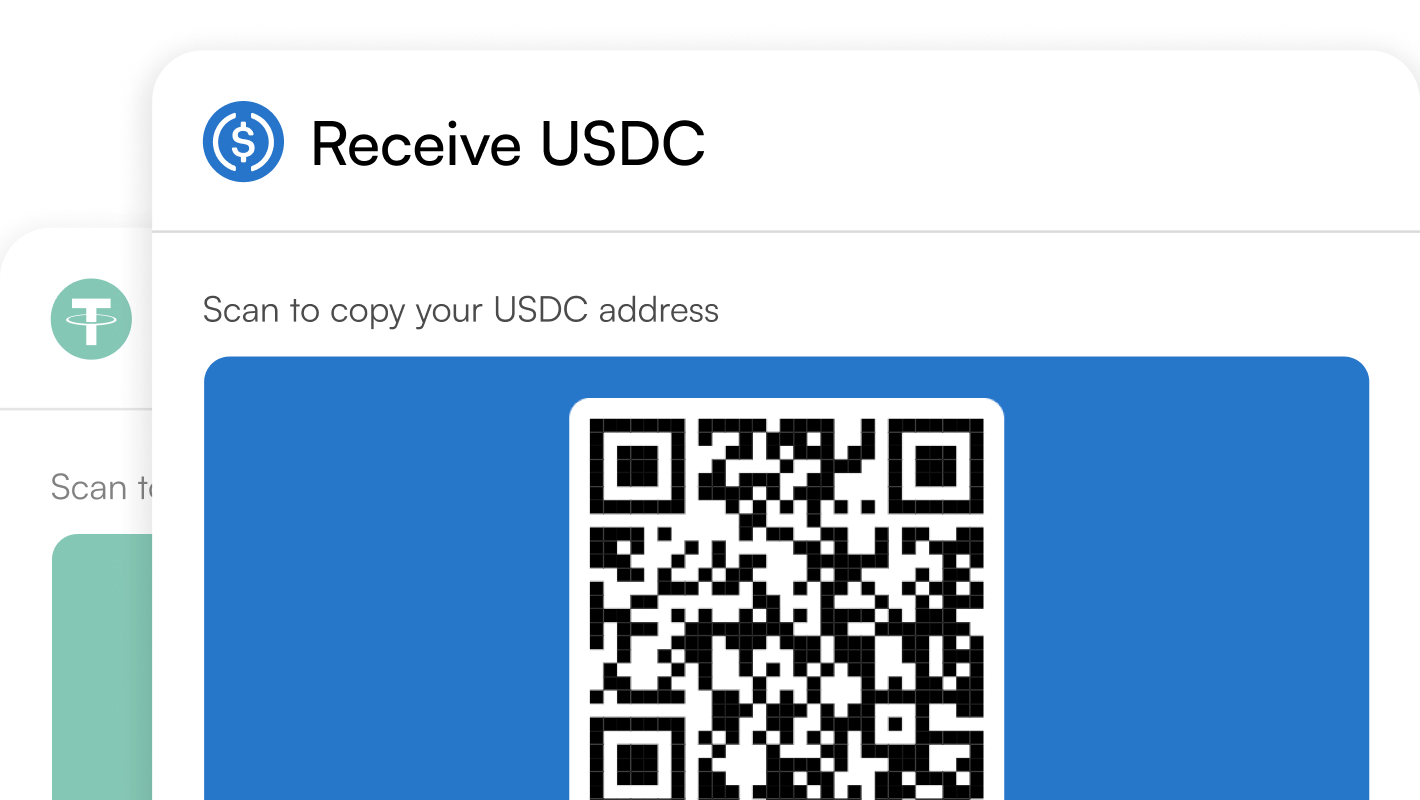

Receive Stablecoin Payments

Accept stablecoins (USDC & USDT) from global clients to your unique FastStables receiving address.

Get AUD Instantly

Go from stablecoins to AUD instantly and remove delays from your cash flow.

AUD to Bank, Fast

Settle your AUD balance directly to your bank, typically lands on the same day.

Create Custom Invoice Links

Build custom invoices that contain your unique stablecoin receiving address.

Get Paid from Anywhere

Accept stablecoin payments worldwide and settle directly to AUD faster, with lower fees and full control.